Taking LinkedIn down one profession at a time | Founder & CEO @WorkweekInc

Austin, TX

Joined April 2011

- Tweets 10,672

- Following 2,272

- Followers 23,212

- Likes 42,174

Adam Ryan 🤝 retweeted

🤯🤯🤯

I've been reviewing the content for next week's Fintech Takes: Builders Summit and it is blowing my mind.

Beyond excited.

Adam Ryan 🤝 retweeted

Can confirm…

As someone who was there from the beginning and saw my equity conveniently “disappear” overnight… lotta bullshit and dishonesty surrounding The Hustle.

Ask anyone who worked there early days. It’s very disappointing but also kinda sad

Adam Ryan 🤝 retweeted

From what I understand having spoken to people.

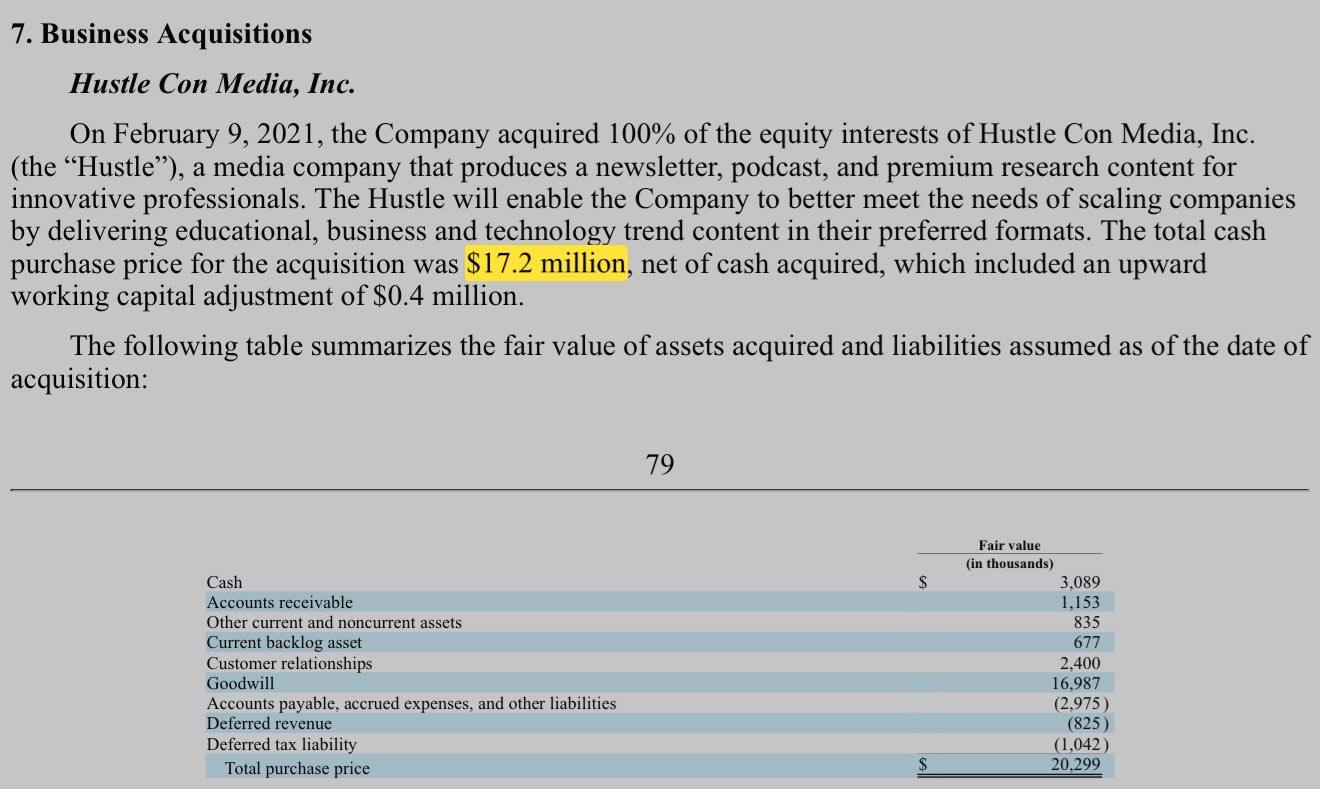

1. The acquisition price was closer to what Jesse says paid in all cash.

2. HUBS gave Sam an employment contract with RSUs, but this wasn’t part of the purchase price.

3. There were also a few other co-founders of Hustle IIRC, so equity was split.

So, $17.2m is likely right + Sam made a ton thanks to HUBS appreciation.

Been waiting for someone to call this out. Jesse is spot on.

So many exaggerations, half truths, and sometimes out right lies told about the founding, building, and exit of Hustle Con Media Inc.

The more you dig…

Years of preparation by these two culiminated into overnight success.

Amazing to watch @jordihays and @johncoogan live out their dream.

i love what i get to do every day. wake up and jump out of bed excited for the day. feel incredibly lucky.

RT @arihappywick: MAJOR LIFE UPDATE:

How do I put 4 years of my life into words?

I worked at Sharma Brands for longer than I was in colle…

Adam Ryan 🤝 retweeted

Smart people doing smart things. Nice work @AdamRy_n !

Adam Ryan 🤝 retweeted

Workweek is building Doximity for every industry beyond Doctors

Huge opportunity- listen to co-founder @AdamRy_n give the @workweekinc pitch on the @tbpn pod

WW is a @LightShedVC portfolio co

Adam Ryan 🤝 retweeted

@AdamRy_n on @tbpn — making sure all of Silicon Valley knows how cool b2b media is and always will be

Morning. On today's show:

– @BBBaumgartner (Ramp)

– @zachperret (Plaid)

– @ewittman (VSCO)

– @panos_panay (Amazon)

– @adamry_n (Workweek)

– @aditabrm (Reducto)

– @vrjbndr (Finch)

– @colintluce (Basis Theory)

– @john__glasgow (Campfire)

– @danshipper (Every)

See you there.

Office for the day

Morning. On today's show:

– @BBBaumgartner (Ramp)

– @zachperret (Plaid)

– @ewittman (VSCO)

– @panos_panay (Amazon)

– @adamry_n (Workweek)

– @aditabrm (Reducto)

– @vrjbndr (Finch)

– @colintluce (Basis Theory)

– @john__glasgow (Campfire)

– @danshipper (Every)

See you there.

Morning. On today's show:

– @BBBaumgartner (Ramp)

– @zachperret (Plaid)

– @ewittman (VSCO)

– @panos_panay (Amazon)

– @adamry_n (Workweek)

– @aditabrm (Reducto)

– @vrjbndr (Finch)

– @colintluce (Basis Theory)

– @john__glasgow (Campfire)

– @danshipper (Every)

See you there.

This is insane. Any other company with this reach is worth a trillion+.

I assume this does not include their API activity. Which gives them fairly unprecedented engagement across consumer and B2B.

I don’t understand the comments about this business failing. Objectively, this has the fundamentals to be an incredible business.

- Burn $8.5B to add $6B in top line.

- Rule of 40 is right around 40. With a product that requires huge capex and has incredible gross margins long term.

- 1B weekly active users gives them n of 1 distribution to expand ARPU through additional products and services.

Is $500B crazy expensive? Yes. Will this company be worth trillions one day? More likely yes than no based off this update.

OpenAI's financial situation (via The Information)

•Revenue: $4.3B in H1 2025 (+16% vs all of 2024).

•Losses: Operating loss $7.8B, net loss $13.5B (over half from remeasurement of convertible equity).

•Cash burn: $2.5B in H1 2025; projected $8.5B for full year.

•R&D: Biggest expense, $6.7B in H1 2025 (on track to double vs 2024).

•Stock compensation: ~$2.5B in H1 (nearly doubled YoY); targeting ~$6B for full year.

•Sales & marketing: $2B in H1 (almost double all of 2024; includes a Super Bowl ad).

•Microsoft: 20% revenue share; projected to save $50B by 2030 as this percentage declines.

•Server costs: $2.5B cost of revenue in H1, mainly renting Nvidia-powered servers via Microsoft.

•Cash reserves: $17.5B in cash + securities at end of Q2; +$10B new funding in June; seeking +$30B in July.

•Valuation: Tender offer values OpenAI at ~$500B (vs $260B at start of 2025).

•Long-term projections: $200B revenue in 2030, $115B cash burn until then, $450B server costs (mostly rented).

•Nvidia deal: LOI for $10B per 1 GW data center capacity (up to $100B).

•User targets: 1B weekly ChatGPT users by end of 2025 (vs 500M in March).

In short: explosive revenue growth, but even higher losses and cash burn, driven by R&D, server costs, and stock comp. Valuation is soaring, while the roadmap assumes massive investment and scale.

I just watched our designer and engineer talk through a large problem IRL. the designer jumped on the engineer's computer. started typing into Claude. engineer would give feedback while she did it.

2 hours later. problem solved.

i hear "this would have been days or even a week of time before"

we're in a new world.

For anyone who has this reaction / thought about Substack. Think again.

Margin gets cut by 50%+ for writers who get paying subs via in-app purchases.

This hurts writers, but helps VCs who want to chase growth metrics (in this case, net-new paying users📈regardless of profitability per user).

Calling it now: the platform is a great arbitrage opportunity for reaching readers in the ecosystem, but the beginning of the end for long-term paid newsletters to flourish. Anyone big will eventually move off-platform and just take their readers' email addresses with them.

You have 2-4 years of reach arbitrage here and then it'll be over. Capitalize while you can.