Dutch global investor & entrepreneur. Founded many companies, among others Tudou.com & Hut 8 Corp. Advisor @ReformDAO & Amdax. Main focus on BTC & AI

Joined July 2014

- Tweets 1,654

- Following 1,643

- Followers 133

- Likes 727

TheMarc Van der Chijs retweeted

Understanding Bitcoin is an IQ test. Understanding Tesla is an even greater one — and very few can pass them both.

TheMarc Van der Chijs retweeted

Unpopular opinion: despite the fact that I lost a lot of money because of SBF, I still believe the lawyers are more too blame for the FTX bankruptcy than SBF. As I have said here before, SBF made big business mistakes, but FTX was solvent. In an alternate history without CZ (who was trying to kill Binance competitir FTX), SBF would have been a crypto hero.

I was on the FTX UCC for the bankruptcy.

@SBF_FTX is correct. If it weren’t for the bankruptcy lawyers, FTX could have paid us all out in-kind just like the Genesis and Gemini bankruptcies did.

Instead we were dollarized at $16,500 BTC while John J. Ray III paid $1M to each of his newly appointed board members to push through his $42M bonanza bonus package post-confirmation (not part of the bk plan we voted on)

TheMarc Van der Chijs retweeted

Another video of people lining up to buy Gold in Australia. It reminds me of Weimar Germany.

The only time I ever lined up to buy BTC was when the world’s first BTC ATM opened in Vancouver in Nov 2013 (and the photo of me waiting made it onto the front page of the NY Times!).

TheMarc Van der Chijs retweeted

Is this a sign that Gold is close to a blow off top or do people realise the fiat system is not working anymore? Someone should hand these people flyers about digital gold (Bitcoin). Or give them scratch tickets with $5 worth of BTC to get them into crypto.

TheMarc Van der Chijs retweeted

Gold is overbought, not because it is overvalued and will crash soon, but because the fiat system is starting to show serious cracks. Smart and conservative investors are fleeing to safety (Gold), less conservative ones are increasing their Bitcoin positions. This is a sign, ignore it at your own peril.

Now that everyone is making double digit (or more) returns on their stocks, maybe we should start to calculate the returns in Gold instead of USD? I believe most of the returns are simply debasement. I know I can do this in TradingView, but are there any apps that also do this?

I did a podcast with @bramk about among others Bitcoin, AI, and my investment philosophy. I am not doing a lot of interviews anymore, but this was fun and I’m glad I made an exception. Interesting discussion, thanks Bram!

BFM196 w/ @marcvanderchijs is live!⚡️

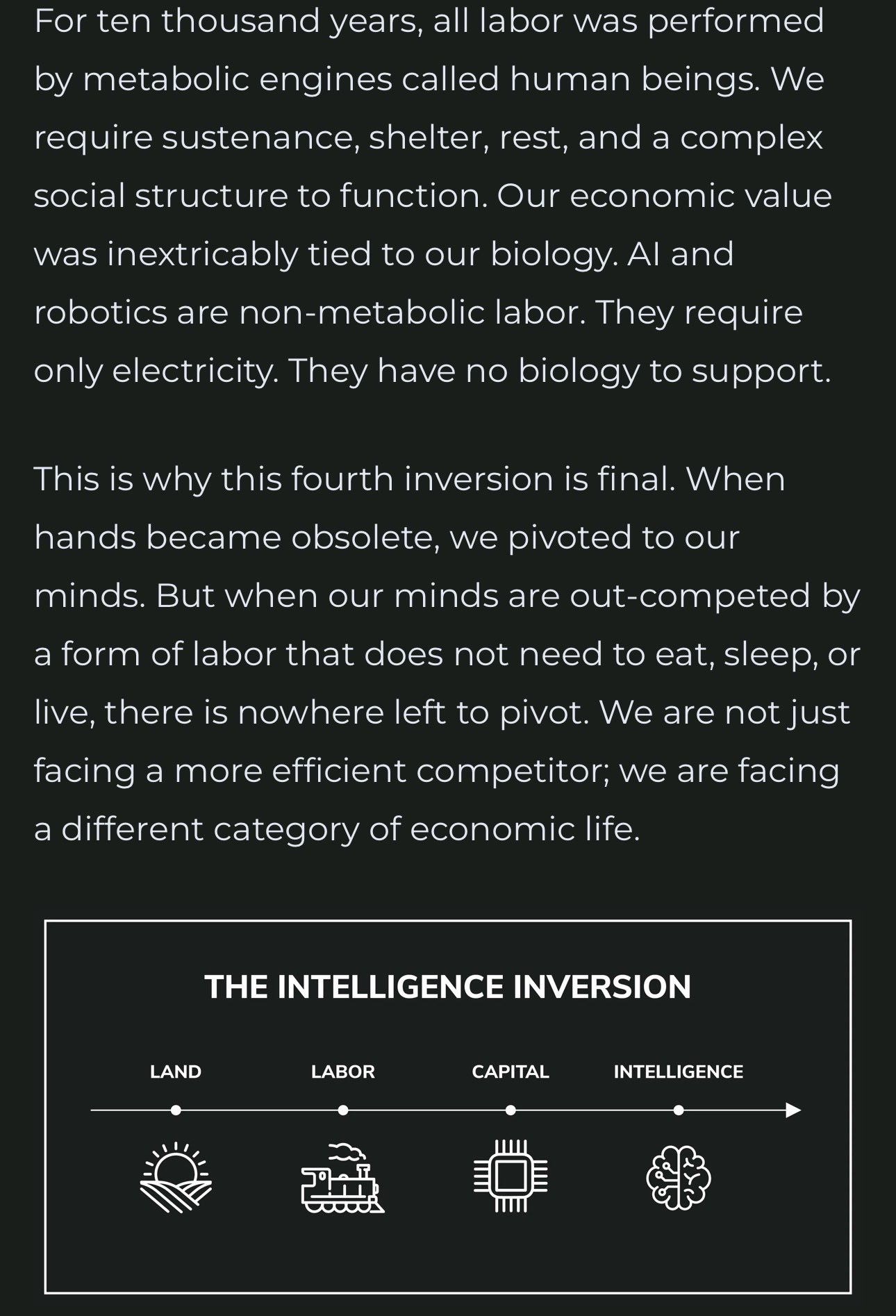

“AI will kill most jobs. Bitcoin will save your future.”

We discuss:

🔸How to discern the future

🔸Why AI needs Bitcoin

🔸How Bitcoin outlasts gold

🔸Why traditional banks will vanish

🔸Bitcoin as the global base layer

🔸The future of work

$1M Bitcoin & AI Dominance: Coming Sooner Than You Think

We discuss how to discern the future in an age of exponential change, why AI needs Bitcoin, how Bitcoin outlasts gold and replaces banks, and what the coming shift means for work, value, and freedom.

TheMarc Van der Chijs retweeted

If you are a $GLXY shareholder you have to follow @RHouseResearch. So much alpha in their tweets. Many other data center investors such as $IREN may not like Rittenhouse for calling these companies out on their financial tricks, but as an investor you should be aware of them.

With all due respect, your take here is ridiculous, especially considering how other "data center developers" in your ETF's portfolio operate.

Helios is a $6.4B project (533MW of critical IT load x $12MM/MW). Assuming 80% LTC (i.e. that Galaxy $GLXY can raise 80%, or $5.3B of the total CapEx bill via project-level debt financing), Galaxy still needs to contribute $1.3B of cash equity into the project. ~$300MM or so has already been funded, resulting in $1B of additional equity capital needed.

Note that $GLXY has already raised $1.4B of non-dilutive project level debt from DB for Phase I (133MW) and is in the market to raise $3.0B for Phase II (260MW). Additional cash in the bank at the HoldCo level ($325MM provided by this deal) will almost certainly help drive better economics on their next project-level debt financing. Also important to note that Galaxy is literally the only crypto x data center developer who has successfully executed project-level debt financing. $WULF, $APLD, $CIFR are all working on it, but none have closed to-date.

While Galaxy has a bigger balance sheet (est. $2B+ of net cash, stablecoins, and liquid assets as of 6/30, but likely materially up when they report Q3) than any other crypto company seeking to build AI data centers, it is still prudent of them to capitalize on the fact that the share price was up 100%+ over the past few months, and ~500% from the April lows. This deal puts an additional $325MM of cash on the balance sheet, providing additional flexibility to invest further in the data center business (for which mgmt. has discussed additional greenfield development opportunities).

In addition, they have a growing, profitable financial services business (investment banking, trading and OTC market making, asset mgmt., lending) that is firing on cylinders . Mgmt. stated July 2025 was the best month in company history. They are rolling out new products and offerings, such as the GalaxyOne app.

Helios involves a significant upfront investment of capital (est. $1.3B total from the $GLXY HoldCo level) but should generate sizeable, stable, recurring cash flows in the very near-term future. Does it really make sense to deplete a significant portion of the capital available on the balance sheet to fund Helios when external capital is clearly available? The dilution is minimal (2.4%), and results in a greater degree of flexibility going forward as they continue to invest in both the data center and digital asset businesses. AI data centers and digital assets are nascent, capital-intensive endeavors - as a $GLXY shareholder, I am a happy to incur minor dilution in exchange for additional flexibility and wiggle-room going forward.

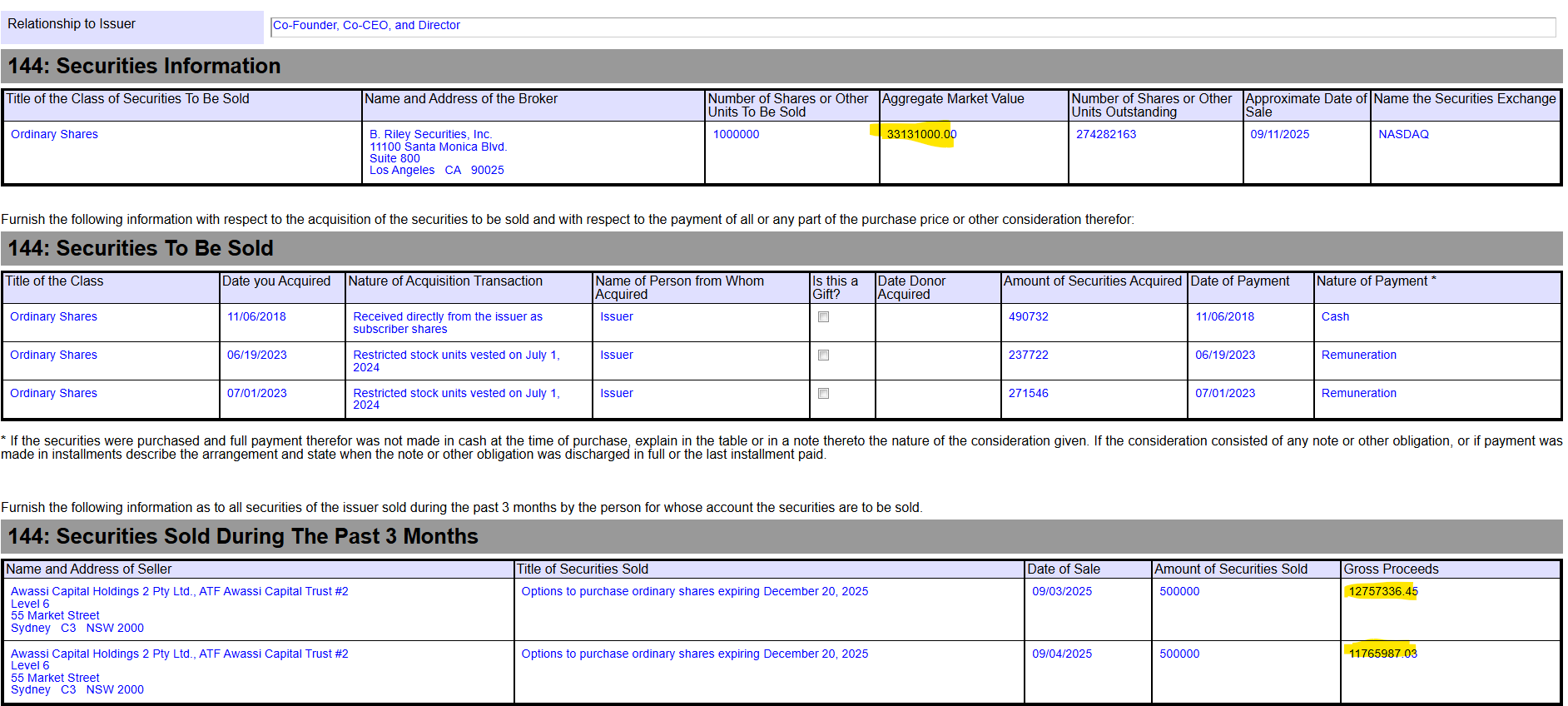

The dilution is not opaque - the press release quite literally tells you that Galaxy is selling 9,027,778 shares. If you then go to the latest 10-Q, you can see on the first page there were 376,287,575 shares outstanding as of July 31, 2025. 9,027,778 divided by 376,287,575 = 2.4%.

With respect to @novogratz selling shares - he has communicated on numerous occasions his intention to bring his ownership down. This is a positive for shareholders for a variety of reasons (i.e. certain investment managers won't touch names with majority shareholders). The fact that his shares are going directly to a large asset manager in connection with a PIPE is a much cleaner way to do this versus a registered underwritten offering - it signals that a large fund has spent extensive time doing diligence on GLXY. Novo is still obviously very well incentivized given his still majority ownership in $GLXY. He has been the majority shareholder since 2018, and has delivered for shareholders - he's not allowed to take a few chips off the table?

What's really amusing to me about your stance here is the sheer hypocrisy given what else is in the NODE ETF. Let's take, for example, $IREN, the second largest holding.

In the past 12 months alone, $IREN has raised over $2.9B of dilutive capital ($1.9B of convertible notes and $1B on their ATM). Not a peep from you on this.

Keep in mind - Galaxy raised capital to help them fund the build-out of Helios, which has contracted cash flows via their lease with CoreWeave. IREN diluted shareholders to buy Bitcoin mining ASICs and buy GPUs on spec. $IREN's 10-K literally tells you that they buy GPUs, then try to find customer contracts. To-date, all they have done is buy GPUs - their cloud offering is completely unproven. $IREN does not have a long-term co-location contract. But again, clearly you didn't have an issue with this dilution to fund speculative investments, given $IREN is the second largest holding in NODE.

Just last month, $IREN's co-CEO's each sold $57MM+ of stock and options. This is completely fine, but Novo selling shares is bad?

Keep in mind - $IREN's board (which is more or less controlled by those two co-CEOs, who have outsized influence over the company relative to their actual financial incentives as they are the sole holders of $IREN's two B Class shares which give them 15x the voting power for each ordinary share they hold then otherwise) decided to modify the co-CEO's compensation in May 2025, with $IREN's share price plunging. The BoD (again - both co-CEOs sit on the BoD) removed the performance requirement thresholds to ensure the co-CEOs RSUs would vest no matter what, citing "extraordinary performance... (under) market-wide structural factors and macroeconomic volatility." To summarize, the co-CEOs basically paid themselves 1MM+ shares that they were only supposed to receive if performance criteria were met... when it became clear that the performance criteria would NOT be met. And then not even 6 months later both co-CEOs sold a corresponding amount of shares. Seems like a great deal for $IREN shareholders!

What's most amusing here is that $IREN's BoD cited "increased power capacity" and "scaled AI Cloud Services capacity to approximately 1,900 Nvidia GPUs" as "key highlights" for the mgmt. team in FY25. Not a peep about customers, profit, return on invested capital, or anything of the nature of actually driving durable, sustainable value to shareholders.

As a result of this, $IREN shares outstanding are up a whopping 50% in the past year, and they still do NOT have any long-term contracted revenue. You claim to be hyper-focused on corporate governance yet have never said a peep about the insanities taking place at NODE's 2nd largest holding. The hypocrisy is astounding.

One last note worth mentioning - Galaxy actually bought back 10.6MM shares in 2022 at ~$5/shr. Seems like good business to buy at ~$5 and sell at $36. Has $IREN, or any other crypto-company within NODE ever returned capital to shareholders via buybacks or dividends? $IREN certainly has not, and I highly doubt any others have either.

Good information, I was wondering about this as well.

I remain very bullish for the remainder of Q4. But I am glad I hardly use any leverage nor invest in low-quality alts, so these shake outs don’t have any real impact on me.

The stock market and crypto crash remind me of early April when Trump announced his tariffs. Don’t freak out, there is so much liquidity in the market that this is a time to buy. We’ll be back at new ATHs soon.

TheMarc Van der Chijs retweeted

Super impressive move from Tesla FSD v14. No other self driving system even comes close, this is how an experienced human driver would drive. With a Tesla there is no need for a chauffeur anymore. The best thing? This will be now available for everyone in the US.

This is the part of the bull market that I enjoy most. It reminds me of 2017 & 2021, with the difference that retail isn't really part of it yet. I haven't seen any Uber drivers with their crypto apps open, once that starts to happen I may start to take some money off the table

This is HUGE: Galaxy Digital just launched a competitor to Robinhood! Stock is up 9% pre market. I just tried to sign up, but it's only for the US for now (I could use a VPN & my US mobile number, but will wait a bit).

One platform. One portfolio. Institutional strength designed to give individuals an edge.

Get GalaxyOne. Now available on web, iOS, and Android: one.galaxy.app/sign-up

The EU is on the verge of becoming a police state without any privacy, and its citizens don’t seem to care.

We are alarmed by reports that Germany is on the verge of a catastrophic about-face, reversing its longstanding and principled opposition to the EU’s Chat Control proposal which, if passed, could spell the end of the right to privacy in Europe.

signal.org/blog/pdfs/germany…

People investing in this are simply greedy and have FOMO. Chamath scammed so many with his SPACs in the past, but he is still able to pull off this deal (at least without warrants this time). There is too much money being printed, this is the result of it.

CHAMATH ANNOUNCES HIS SPAC RETURN WITH $AEXA:

Some details he announced today:

- A SPAC has been successfully priced without warrants, with the sponsor’s compensation entirely tied to stock price appreciation.

- AEXA was more than 5x oversubscribed with $1.4B in demand, resulting in an upsizing to $345M.

- The gap between private and public markets has widened, with over 700 U.S. private companies valued above $1B compared to 150 in 2017, complicating liquidity for employees’ paper wealth and reinvestment for early investors.

So seems like there is pretty strong demand for the SPAC, Chamath thinks that too many companies are staying public which is why this is the right time to bring back the SPACs thesis, and his compensation is tied to the share price of the SPAC being successful.

Would you take a chance with his newest SPAC?

Finally finished Secret of Secrets (I always read 3-4 books at the same time, on average I read 1 book/week). Good story and lots of food for thought (does life end at death?), but the end was too much "USA, USA, USA!". Not sure if that still works for international audiences.

TheMarc Van der Chijs retweeted

While Wall Street focuses on the next 12-18 months retail investors can focus on the next 2-3 years. You can front run Wall Street —> this is your advantage.

TheMarc Van der Chijs retweeted

The world of investing has changed a lot over the past couple of years, with Asia leading the way. I actually think this could be successful with young people in the Western world as well. You could build a cool format around it where fans can bet on who will win and get a percentage of the profits (either IRL or online).